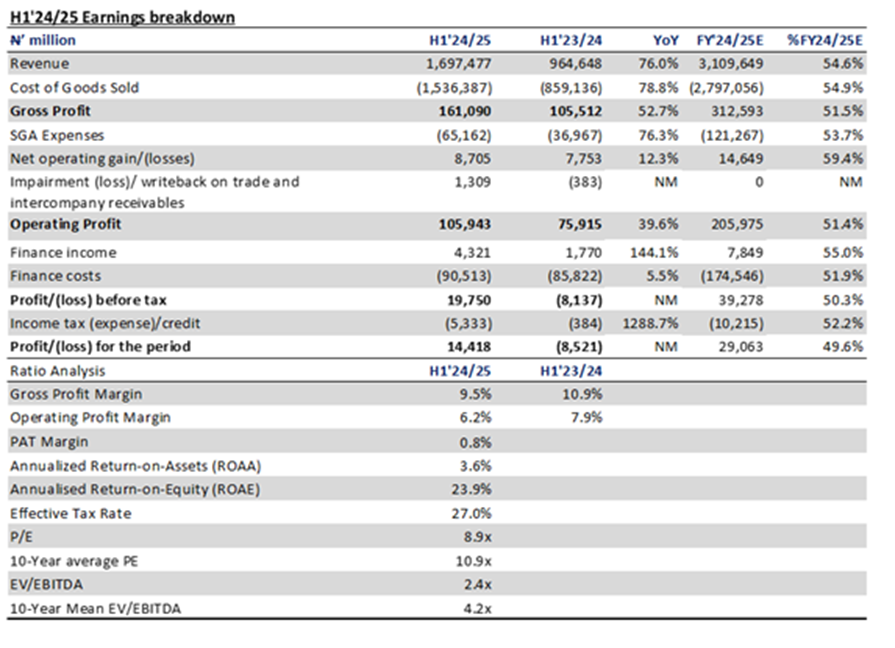

Revenue grew by 76.0% to N1.70 trillion, buoyed by growth across its business segments Food (+74.5%), Sugar (+83.75%), Agro-allied (+75.2%), and Support (+71.3%). Elsewhere, the cost of production rose by 78.8%, driven by increases in material (+80.5%) and power (+113.1%) expenses.

Further down, the company recorded operating profit growth of 39.6% to N105.94bn; however, the EBIT margin contracted by 1.6 ppts to 6.2%, following a 76.3% increase in operating expense.

FLOURMILL recorded a 2.6% increase in net finance cost as interest on borrowings rose. Additionally, exchange losses declined by 9.1% to 46.55bn as the naira was relatively stable during the period. Thus, PBT rose to 19.75bn (from a negative N8.14bn in 9M’2023). The company incurred a tax expense of N5.33bn; hence, PAT settled at N14.42bn (from a negative N8.52bn in the corresponding period last year).

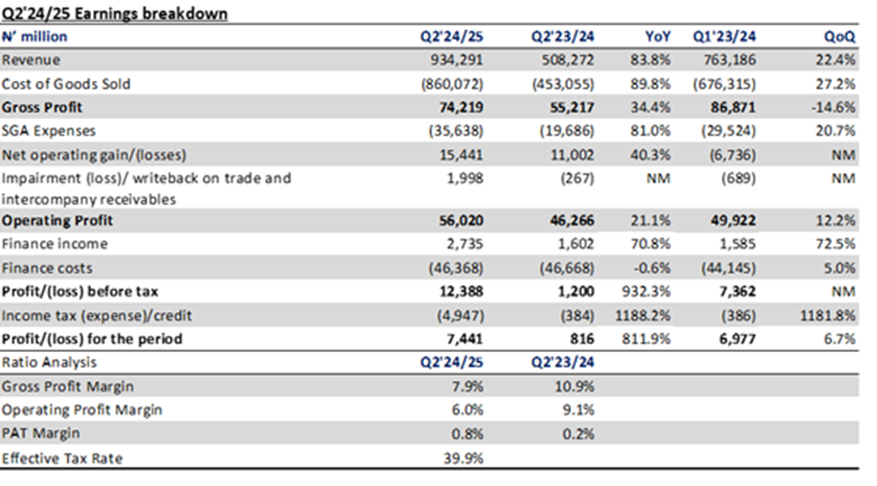

In its Q2’2024/2025 performance, revenue grew by 83.8% YoY, whereas cost of sales increased by 89.8%. Hence, the gross margin declined by 2.9ppts to 7.9% (vs 10.9% in Q2’2024/2025).

Despite an increase in operating expenses (+81.0%), operating profit increased by 21.1% owing to a rise in net operating gain (+40.3%) and writeback on trade and intercompany receivables (N15.44bn).

Finance income went up by 70.8% to 2.74bn, driven by interest on financial instruments. On the other hand, finance costs declined marginally by 0.6%. Overall, PAT rose by 9.12x to N7.44bn.

{kind=link}